Alpha is a function of risk management

Active management involves tactical decision making by the manager that aims to produce better risk adjusted returns in relation to a relevant benchmark. Active management may involve stock picking and asset allocation decisions which has the potential to add value or not. It has become increasingly difficult for stock pickers over the past decade to add significant value in relation to their passive counterparts. It is our view that active management will become increasingly important going forward given that it is focused more on risk management than instrument selection. Our way of adding value is to actively manage market risk within portfolios by hedging directional risk when it makes sense as per our unbiased tactical process. Our concern with active management is therefore solely focused on risk management.

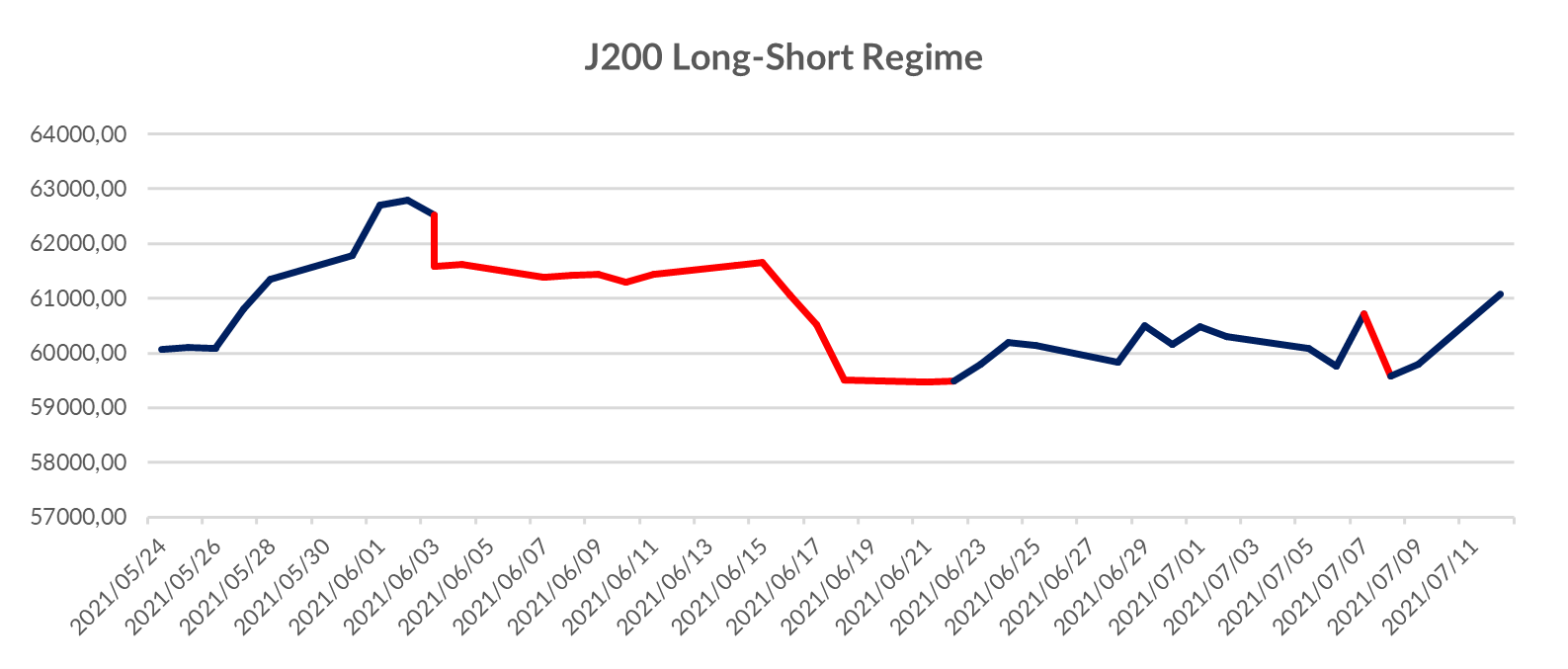

The above graph is an illustration of how the tactical management process is applied. The periods marked in red indicates times where our long Beta position were hedged against downside market risk and the period in blue indicates periods of no hedging and naked long exposure. The periods indicated in red protected our core long beta position and underlines the way in which we intend to add value in our portfolios.

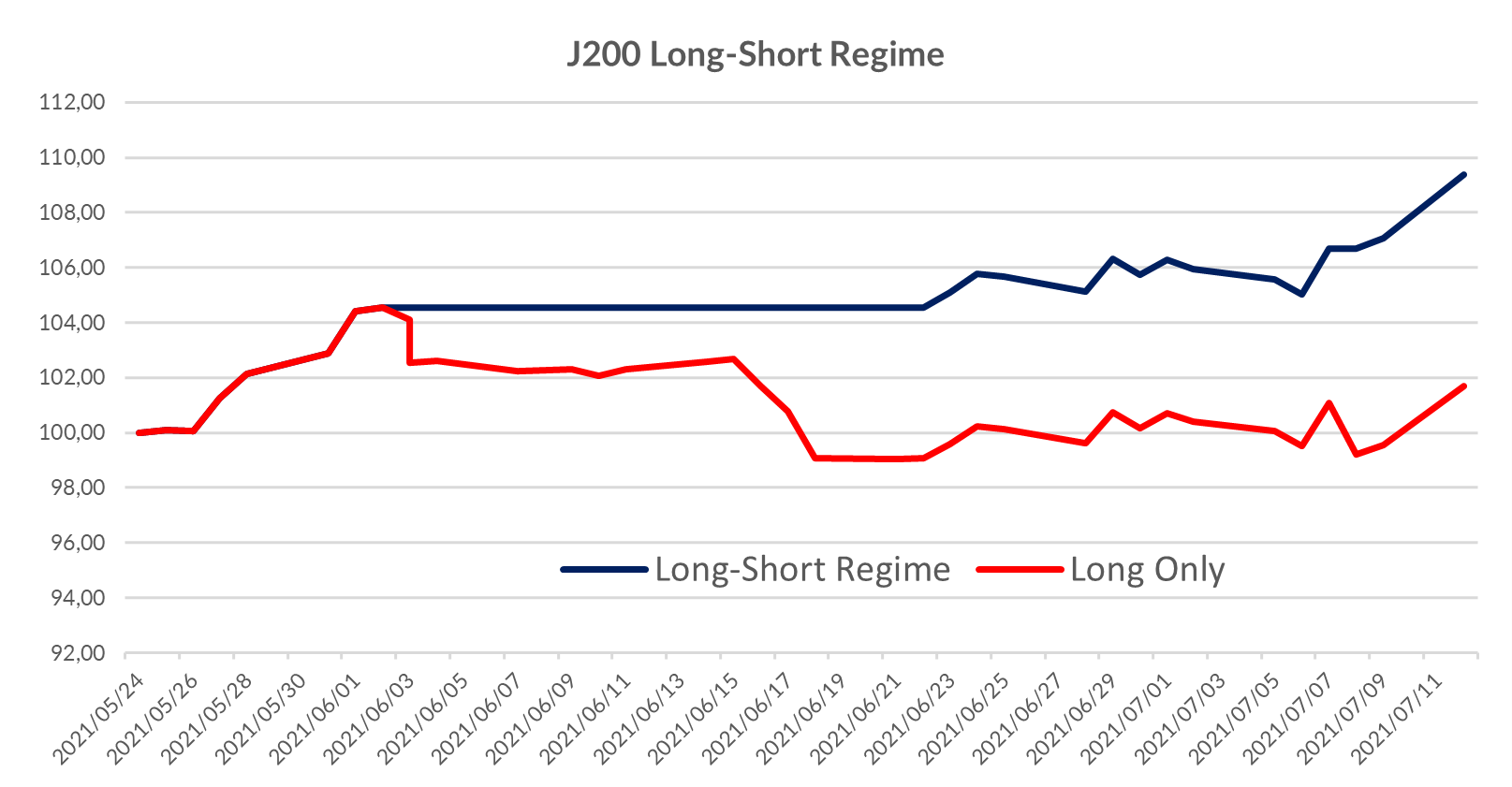

The above graph illustrates the cumulative effect that our active management regime had in relation to the market portfolio. The difference between the blue and red graph is active management and it can be stated with confidence that it is pure alpha. It is also important to note that the outperformance (Alpha) in the above illustration was as a function of risk management.